Futures Market: Overnight, LME copper opened at $9,559.5/mt, bottomed at $9,508/mt during early trading, and then moved higher, peaking at $9,594.5/mt by the session close. It finally settled at $9,594/mt, up 2.21%, with a trading volume of 33,000 lots and an open interest of 295,000 lots. Meanwhile, the most-traded SHFE copper 2504 contract opened at 77,980 yuan/mt, quickly peaked at 77,990 yuan/mt, and fluctuated rangebound throughout the session, bottoming at 77,640 yuan/mt in early trading. It eventually closed at 77,900 yuan/mt, up 1.02%, with a trading volume of 39,000 lots and an open interest of 166,000 lots.

【SMM Copper Morning Brief】News: (1) The Trump administration decided to grant some tariff exemptions to Canada and Mexico, but Canada may not accept them.

On Wednesday, March 5, near midday trading in US stocks, media cited White House officials stating that the US is considering delaying the implementation of auto tariffs on Canada and Mexico by one month. US government officials met with executives from three major automakers—Ford, General Motors, and Stellantis NV—on Tuesday to discuss the matter. A meeting on potential tariff reductions was scheduled at the White House on Wednesday.

(2) On the afternoon of March 5, Xi Jinping, General Secretary of the CPC Central Committee, President of China, and Chairman of the Central Military Commission, emphasized during a review session with the Jiangsu delegation at the third session of the 14th National People's Congress that major economic provinces must take the lead in achieving the goals of the 14th Five-Year Plan. Jiangsu should focus on key areas, lead in integrating technological and industrial innovation, pioneer in deepening reforms and high-level opening-up, take the forefront in implementing major national development strategies, and set an example in promoting common prosperity for all people.

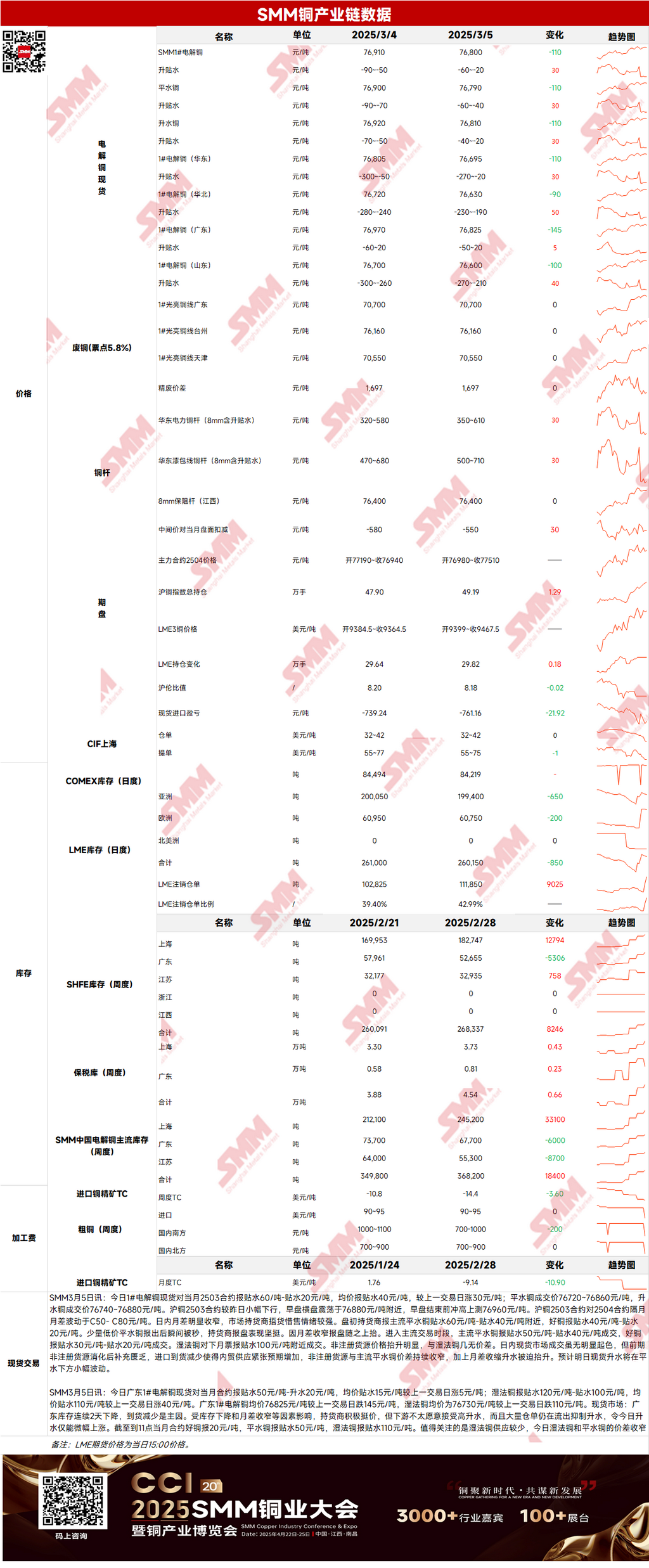

Spot Market: (1) Shanghai: On March 5, #1 copper cathode spot prices against the front-month 2503 contract were quoted at a discount of 60 yuan/mt to 20 yuan/mt, with an average price at a discount of 40 yuan/mt, up 30 yuan/mt from the previous trading day. Although spot market transactions showed no significant improvement, the depletion of non-registered cargoes led to a lack of replenishment, and reduced imports heightened expectations of tight domestic supply. The price spread between non-registered cargoes and standard-quality copper continued to narrow, and the shrinking price spread between futures contracts forced spot premiums to rise. Spot premiums are expected to fluctuate slightly below parity today.

(2) Guangdong: On March 5, #1 copper cathode spot prices against the front-month contract were quoted at a discount of 50 yuan/mt to a premium of 20 yuan/mt, with an average price at a discount of 15 yuan/mt, up 5 yuan/mt from the previous trading day. Overall, narrowing inventories and price spreads between futures contracts supported premiums, but downstream restocking demand remained weak, resulting in only a slight increase in spot premiums.

(3) Imported Copper: On March 5, warehouse warrant prices ranged from $32 to $42/mt, QP March, with the average price unchanged MoM. B/L prices ranged from $55 to $75/mt, QP April, with the average price down $1/mt MoM. EQ copper (CIF B/L) prices ranged from -$2/mt to $6/mt, QP March, with the average price up $2/mt MoM. Quotes referenced cargoes arriving in mid-to-late March. After significant transactions of warehouse warrants in the earlier period, B/L trading in the spot market returned to a subdued state. Buyers focused on EQ cargoes arriving in late March, with offers slightly recovering compared to earlier levels.

(4) Secondary Copper: On March 5, secondary copper raw material prices remained unchanged MoM. Guangdong bare bright copper prices were 70,600-70,800 yuan/mt, unchanged from the previous trading day. The price difference between primary metal and scrap was 1,697 yuan/mt, unchanged MoM. The price difference between primary and secondary copper rods was 1,030 yuan/mt. According to the SMM survey, late-session copper price surges of 400 yuan/mt occurred. However, as secondary copper rod enterprises had mostly completed their daily procurement by then, it remains to be seen whether the copper price increase will boost secondary copper raw material supply. After the session, US President Trump reiterated plans to impose a 25% tariff on aluminum, steel, and wood. Following the announcement, COMEX copper and LME copper both rose to varying degrees. If SHFE copper prices follow suit tomorrow, secondary copper raw material supply is expected to increase effectively.

(5) Inventory: On March 5, LME copper cathode inventory decreased by 850 mt to 260,150 mt. SHFE warrant inventory decreased by 1,014 mt to 160,775 mt.

Prices: On the macro side, Trump’s further delay of some tariffs heightened concerns about inflation and the economy, leading to a continuous decline in the US dollar index, which hit a nearly four-month low, falling below the 105 mark and supporting copper prices. Domestically, the Two Sessions emphasized stabilizing the real estate and stock markets for the first time in the government work report, along with other favorable policies, significantly boosting copper prices. On the fundamentals side, narrowing price spreads between futures contracts, reduced imports, and heightened expectations of tight domestic supply supported premiums, though downstream transactions showed no significant improvement. Overall, with frequent positive news during the Two Sessions and the US dollar index remaining at low levels, copper prices are expected to remain firm today.

》Click to View the SMM Metal Database

【The above information is based on market data and comprehensive assessments by the SMM research team. The information provided is for reference only and does not constitute direct investment advice. Clients should make prudent decisions and not substitute this information for independent judgment. Any decisions made by clients are unrelated to SMM.】